What many foreign employers overlook is the French concept of prévoyance, a separate but equally crucial pillar of social protection.

What is "Prévoyance" in France?

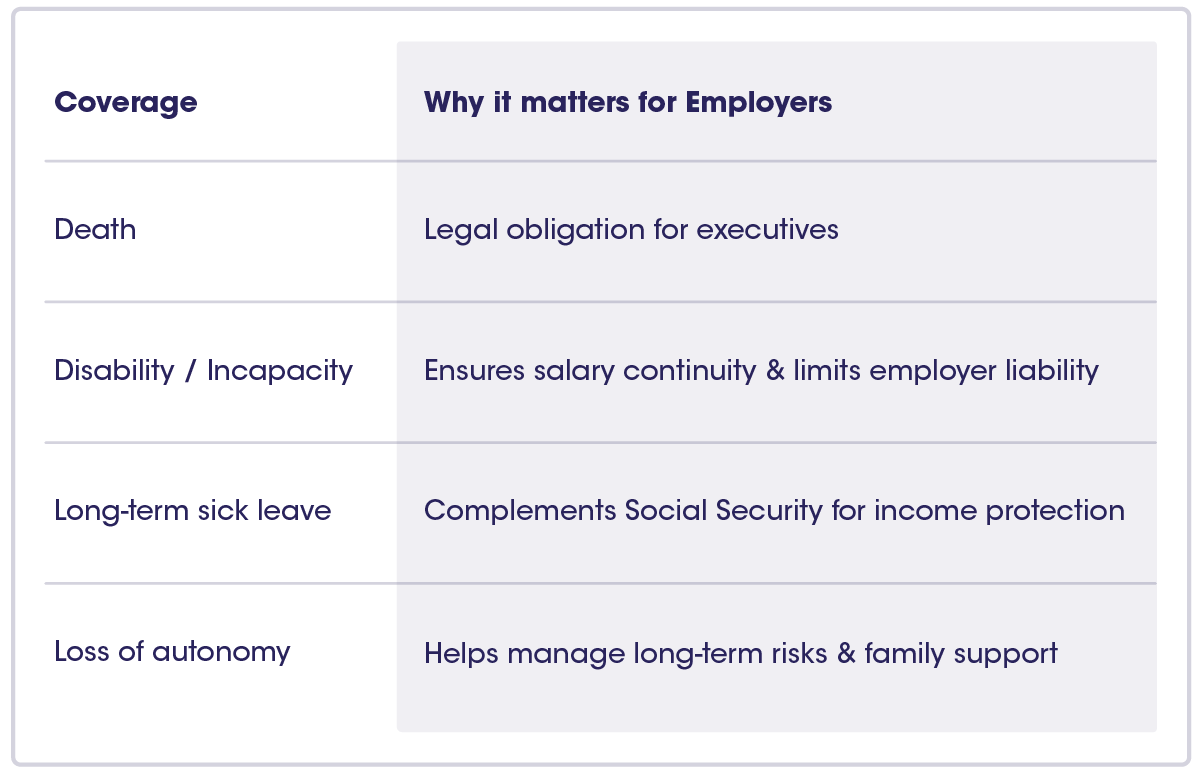

In France, prévoyance provides insurance for major life risks that go beyond everyday healthcare. It complements the basic coverage offered by Social Security, ensuring financial stability when serious events occur.

Typical coverage includes:

- Disability insurance (temporary or permanent)

- Death benefits (lump sum or pension for the family)

- Long-term sick leave compensation

- Loss of autonomy or work capacity

In short: Prévoyance protects employees and their families by maintaining income and dignity when life takes a serious turn.

Why employers should care?

Legal requirements

- For non-executives, group prévoyance is usually optional, though strongly recommended

- For executives (“cadres”), it is mandatory under national collective agreements (e.g., Syntec), which require at least employer-funded death insurance.

Reduced HR and financial risk

Prévoyance plans cover part of income replacement during long-term illness or incapacity, reducing absenteeism risks and legal exposure.

Recruitment and retention advantage

Strong social protection benefits are expected in the French job market. Offering solid prévoyance coverage helps:

- Attract and retain skilled employees

- Strengthen your employer brand

- Avoid unexpected HR crises

Financial benefits

Employer contributions to prévoyance are partially exempt from social charges (within legal ceilings), making it a cost-effective benefit.

How employers can implement "Prévoyance"?

1. Check collective agreement obligations (CCN) in your sector. Some mandate specific coverage levels.

2. Select a group prévoyance plan (via insurer or mutual), covering at minimum death/disability, ideally also sick leave and loss of autonomy.

3. Formalise implementation through a collective agreement or unilateral employer decision.

4. Contribute at least the mandatory minimum (e.g., 1.5% of Tranche A salary for executive death insurance).

5. Report contributions in payroll and monthly DSN (Déclaration Sociale Nominative).

Prevoyance in a nutshell

Key Takeaways

Prévoyance in France is not optional—it’s both a legal requirement (for executives) and a strategic HR tool for all employers.